Investor Letters leverages the Visible platform to surface insightful stakeholder updates sent from leaders of public and private companies as well as top asset managers, venture capitalists, and product and business thinkers. Subscribe and receive a new investor letter, supplemented with Visible charts and actionable insight every Wednesday.

Amazon Before it Was Amazon

It might be the most well-known (and prescient) investor letter in the history of the technology industry so we will keep this week’s intro short. Jeff Bezos’ 1997 letter to Amazon shareholders is truly a master class in building a business – in 1997, 2016 or undoubtedly any date before or after.

We have added a bunch of notes below (anything you see in bold, in quotes, or presented as visualizations was added by us) to help showcase how Amazon has delivered on the promises made in this letter.

The Investor Letter

To our shareholders:

Amazon.com passed many milestones in 1997: by year-end, we had served more than 1.5 million customers, yielding 838% revenue growth to $147.8 million, and extended our market leadership despite aggressive competitive entry.

But this is Day 1 for the Internet and, if we execute well, for Amazon.com. Today, online commerce saves customers money and precious time. Tomorrow, through personalization, online commerce will accelerate the very process of discovery. Amazon.com uses the Internet to create real value for its customers and, by doing so, hopes to create an enduring franchise, even in established and large markets.

“Day 1” – Amazon has grown of age alongside the global Internet, as a vast majority of new Internet users have come online during Amazon’s lifetime.

We have a window of opportunity as larger players marshal the resources to pursue the online opportunity and as customers, new to purchasing online, are receptive to forming new relationships. The competitive landscape has continued to evolve at a fast pace. Many large players have moved online with credible offerings and have devoted substantial energy and resources to building awareness, traffic, and sales. Our goal is to move quickly to solidify and extend our current position while we begin to pursue the online commerce opportunities in other areas. We see substantial opportunity in the large markets we are targeting. This strategy is not without risk: it requires serious investment and crisp execution against established franchise leaders.

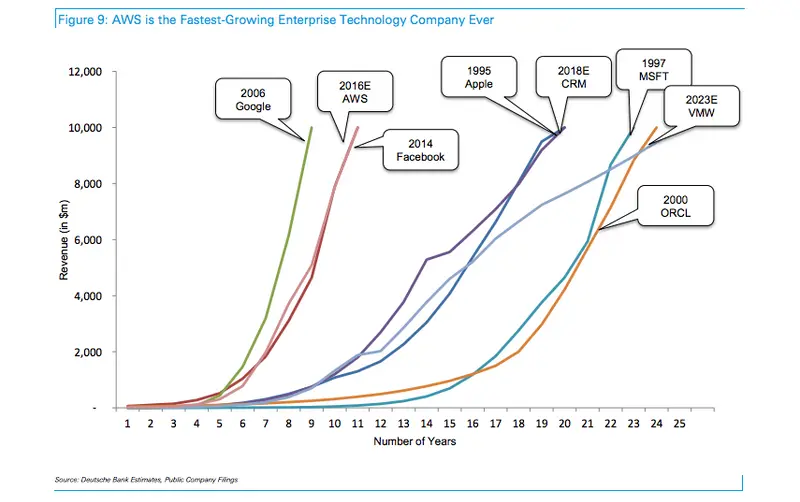

One of the most amazing things Amazon has done in the almost 20 years since this letter is turn investments they were making to improve their core business – heavy spending on infrastructure – into a multi-billion dollar business of its own, AWS. There were (and still are) major players in the cloud infrastructure space that Amazon was going straight up against but that hasn’t stopped the rapid growth of AWS. According to Deutsche Bank, AWS as a standalone entity would be one of the fastest growing enterprise tech companies ever.

It’s All About the Long Term

We believe that a fundamental measure of our success will be the shareholder value we create over the long term. This value will be a direct result of our ability to extend and solidify our current market leadership position. The stronger our market leadership, the more powerful our economic model. Market leadership can translate directly to higher revenue, higher profitability, greater capital velocity, and correspondingly stronger returns on invested capital.

This idea – the Amazon flywheel – brilliantly illustrates the way that Jeff Bezos and his team see all of these factors building on and feeding into one another. Note, as Benedict Evans did here, that there is no outward arrow titled “take profits”.

Our decisions have consistently reflected this focus. We first measure ourselves in terms of the metrics most indicative of our market leadership: customer and revenue growth, the degree to which our customers continue to purchase from us on a repeat basis, and the strength of our brand. We have invested and will continue to invest aggressively to expand and leverage our customer base, brand, and infrastructure as we move to establish an enduring franchise.

That customer base expansion focus? It is going pretty well.

Because of our emphasis on the long term, we may make decisions and weigh tradeoffs differently than some companies. Accordingly, we want to share with you our fundamental management and decision-making approach so that you, our shareholders, may confirm that it is consistent with your investment philosophy:

We will continue to focus relentlessly on our customers.

- We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.

- We will continue to measure our programs and the effectiveness of our investments analytically, to jettison those that do not provide acceptable returns, and to step up our investment in those that work best. We will continue to learn from both our successes and our failures.

While they are not as well known as Google for launching and then quickly shuttering projects, Amazon has certainly lived by the philosophy they espouse above. The Amazon Fire Phone is just the latest in along line of projects like this.

- We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case.

Amazon’s dominance goes a step beyond simply market leadership. In 2015, Amazon accounted for $0.51 of every incremental $1.00 spent online and are now responsible for almost a quarter of all retail growth in the United States.

- We will continue to focus on hiring and retaining versatile and talented employees, and continue to weight their compensation to stock options rather than cash. We know our success will be largely affected by our ability to attract and retain a motivated employee base, each of whom must think like, and therefore must actually be, an owner.

We aren’t so bold as to claim that the above is the “right” investment philosophy, but it’s ours, and we would be remiss if we weren’t clear in the approach we have taken and will continue to take.

With this foundation, we would like to turn to a review of our business focus, our progress in 1997, and our outlook for the future.

Obsess Over Customers

From the beginning, our focus has been on offering our customers compelling value. We realized that the Web was, and still is, the World Wide Wait. Therefore, we set out to offer customers something they simply could not get any other way, and began serving them with books. We brought them much more selection than was possible in a physical store (our store would now occupy 6 football fields), and presented it in a useful, easy-to search, and easy-to-browse format in a store open 365 days a year, 24 hours a day. We maintained a dogged focus on improving the shopping experience, and in 1997 substantially enhanced our store. We now offer customers gift certificates, 1-Click(SM) shopping, and vastly more reviews, content, browsing options, and recommendation features. We dramatically lowered prices, further increasing customer value. Word of mouth remains the most powerful customer acquisition tool we have, and we are grateful for the trust our customers have placed in us. Repeat purchases and word of mouth have combined to make Amazon.com the market leader in online bookselling.

By many measures, Amazon.com came a long way in 1997:

- Sales grew from $15.7 million in 1996 to $147.8 million — an 838% increase

- When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.

- We will share our strategic thought processes with you when we make bold choices (to the extent competitive pressures allow), so that you may evaluate for yourselves whether we are making rational long-term leadership investments.

- We will work hard to spend wisely and maintain our lean culture. We understand the importance of continually reinforcing a cost-conscious culture, particularly in a business incurring net losses.

- We will balance our focus on growth with emphasis on long-term profitability and capital management. At this stage, we choose to prioritize growth because we believe that scale is central to achieving the potential of our business model.

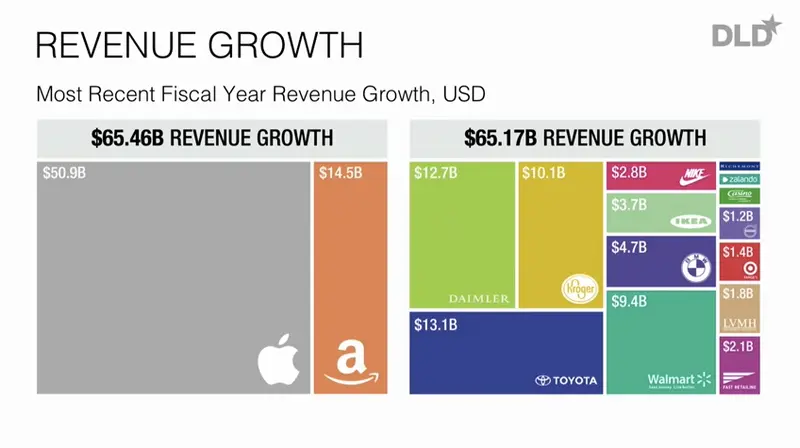

The focus on growth remains, as evidenced by the chart just below. And the second image, highlighting the growth of Apple and Amazon relative to other massive multinational businesses drives home the point of just how successful that focus remains today.

- Cumulative customer accounts grew from 180,000 to 1,510,000 — a 738% increase.

- The percentage of orders from repeat customers grew from over 46% in the fourth quarter of 1996 to over 58% in the same period in 1997.

- In terms of audience reach, per Media Metrix, our Web site went from a rank of 90th to within the top 20.

- We established long-term relationships with many important strategic partners, including America Online, Yahoo!, Excite, Netscape, GeoCities, AltaVista, @Home, and Prodigy (Ed note: Look at those names!)

Infrastructure

During 1997, we worked hard to expand our business infrastructure to support these greatly increased traffic, sales, and service levels:

- Amazon.com’s employee base grew from 158 to 614, and we significantly strengthened our management team. (Ed Note: Now over 230,000 employees)

- Distribution center capacity grew from 50,000 to 285,000 square feet, including a 70% expansion of our Seattle facilities and the launch of our second distribution center in Delaware in November.

- Inventories rose to over 200,000 titles at year-end, enabling us to improve availability for our customers.

- Our cash and investment balances at year-end were $125 million, thanks to our initial public offering in May 1997 and our $75 million loan, affording us substantial strategic flexibility.

Our Employees

The past year’s success is the product of a talented, smart, hard-working group, and I take great pride in being a part of this team. Setting the bar high in our approach to hiring has been, and will continue to be, the single most important element of Amazon.com’s success.

It’s not easy to work here (when I interview people I tell them, “You can work long, hard, or smart, but at Amazon.com you can’t choose two out of three”), but we are working to build something important, something that matters to our customers, something that we can all tell our grandchildren about. Such things aren’t meant to be easy. We are incredibly fortunate to have this group of dedicated employees whose sacrifices and passion build Amazon.com.

Unless you’ve been living under a rock for the last couple of years, you are probably well aware of the PR issues the company faces in the wake of a major New York times investigation into its corporate culture. Here a a few select quotes.

Goals for 1998

We are still in the early stages of learning how to bring new value to our customers through Internet commerce and merchandising. Our goal remains to continue to solidify and extend our brand and customer base. This requires sustained investment in systems and infrastructure to support outstanding customer convenience, selection, and service while we grow. We are planning to add music to our product offering, and over time we believe that other products may be prudent investments. We also believe there are significant opportunities to better serve our customers overseas, such as reducing delivery times and better tailoring the customer experience. To be certain, a big part of the challenge for us will lie not in finding new ways to expand our business, but in prioritizing our investments.

We now know vastly more about online commerce than when Amazon.com was founded, but we still have so much to learn. Though we are optimistic, we must remain vigilant and maintain a sense of urgency. The challenges and hurdles we will face to make our long-term vision for Amazon.com a reality are several: aggressive, capable, well-funded competition; considerable growth challenges and execution risk; the risks of product and geographic expansion; and the need for large continuing investments to meet an expanding market opportunity. However, as we’ve long said, online bookselling, and online commerce in general, should prove to be a very large market, and it’s likely that a number of companies will see significant benefit. We feel good about what we’ve done, and even more excited about what we want to do.

1997 was indeed an incredible year. We at Amazon.com are grateful to our customers for their business and trust, to each other for our hard work, and to our shareholders for their support and encouragement.

/s/ JEFFREY P. BEZOS

Jeffrey P. Bezos

Founder and Chief Executive Officer

Amazon.com, Inc.

Further Reading on the Rise of Amazon

- This video from NYU professor Scott Galloway gives an awesome look at the dominance of Amazon and its fellow behemoths Google, Apple, and Facebook. We used a couple of graphics from his presentation above.

- The AWS IPO by Ben Thompson. In fact, go read anything Ben writes — about Amazon or anyone.

- Why Amazon Has No Profits (and Why it Works) by A16Z’s Benedict Evans