What is a Convertible Note?

A convertible note is a type of short term debt that converts into equity. Convertible note holders essentially get paid interest in the form of discounted equity shares, rather than regularly scheduled payments. They are often used by early stage startups when closing a seed round, and later stage companies looking for more cash in a ‘bridge’ round before their next planned fundraise. Convertible notes have a few key components:

Conversion Discount — The discount at which the investor will receive shares at the date of maturity or the next ‘qualified financing’ (i.e. the next round of funding).

Valuation Cap — The cap on the valuation (i.e. price) that the investors will pay for their equity during the company’s next fundraise.

Interest Rate — This interest rate will be added to the principal amount invested when the debt converts into equity. Most convertible notes in 2020 have a low rate to keep the value primarily on the equity conversion & reflect the current interest rate environment.

Maturity Date — Like some other forms of debt, convertible notes have a maturity date at which the investor can request full payment back from the company. This date is mostly designed to set expectations for the date of the next round of funding.

It depends. They have some clear advantages in that they tend to allow deals to get done faster. However, many in the VC community have been critical, citing that they come with more complexity and hidden risk down the road if both sides are not careful.

Related resource: Liquidation Preference: Types of Liquidation Events & How it Works

Are Convertible Notes Good or Bad?

When Convertible Notes Are Good

Convertible notes are good for quickly closing a Seed round. They’re great for getting buy in from your first investors, especially when you have a tough time pricing your company. Paul Graham wrote a post in 2010 called ‘High Resolution Fundraising’ in which he argued that innovation in convertible securities allows for more accurate & personalized pricing in early stage funding. If you need the cash to get you to a Series A that will attract a solid lead investor at a fair price, a convertible note can help.

When Convertible Notes Are Bad

Convertible notes are destructive when used carelessly. Having too many notes or poorly structured notes outstanding can put your company and later negotiations at risk by complicating your cap table. You should partner with a lawyer who understands the ins and outs of convertible notes, and educate yourself prior to closing a round with this type of funding. Convertible notes are great for speed in Seed rounds, but they must be well thought out to avoid problems later on.

What Happens When a Convertible Note Matures?

When a convertible note is issued, both the investor and founders are expecting the debt to ‘mature’ by converting to equity during a financing round within the next 1 to 2 years. However, notes also come with maturity dates, enabling the investor to get their money back (with some interest added to the principal) if that financing round does not happen on time.

There have been instances in which companies are either acquired before their initial equity round or choose to not raise any equity funding. These are both rare occurrences, but they create tough situations. See investors are not making an exceptionally high risk investment just to get their principal back plus a small interest rate. VC’s and angels win by having huge outliers in their portfolio – if they don’t get equity and you become a unicorn, they lose. It’s best for founders to add language into their convertible notes that state what investors can expect to get in these situations.

Do You Have to Pay Back a Convertible Note?

Convertible notes are just like any other form of debt – you’ll need to pay back the principal plus interest. In an ideal world, a startup would never pay back a convertible note in cash. However, if the maturity date hits prior to a Series A financing, investors can choose to demand their money back. This could effectively bankrupt the company. After all, the startup raised the money because they didn’t have the cash in the first place. If a company raises money using multiple convertible notes, this risk is even greater. Because of this, neither side of the table wants a convertible note to reach its maturity date prior to the next round of funding.

Is a Convertible Note Debt or Equity?

Convertible notes begin as short term debt, but convert into equity during a later round of financing by allowing the investor to receive a discount on shares at a future date. The investor technically has downside protection in the event that the company goes out of business until the note converts. They are entitled to their principal in a liquidity event prior to the conversion date, or if the note reaches maturity prior to a qualified financing.

Related Resource: A User-Friendly Guide on Convertible Debt

How Does a Convertible Note Convert?

A convertible note converts at the next ‘qualified financing round.’ In most cases, convertible notes are issued during a seed round, with the Series A round being the expected conversion event. However, it’s critical to understand the terms at which the note will convert because it will have a huge impact on dilution (this article goes into depth on convertible instruments and dilution). There are three options, all of which are explained in great detail in this post from CooleyGo and this one from Alexander Jarvis

Pre Money Method

In this instance, the convertible note converts based on the pre-money Series A valuation of the company. The dilution in this case will be passed from the founders on to the note holders and new Series A investors.

Percent Ownership Method

With this method, the note will convert based the percent ownership that the incoming Series A investor expects to receive. Founders bear the brunt of all of the dilution, which benefits the convertible note holder in addition to the new investor.

Dollars Invested Method

This method is unique in that it includes the value of the convertible note in the post money valuation of the company. In the Pre Money Method, the founder is favored at the expense of investors, while in the Percent Ownership Method, the founder gets diluted more than they expect. The Dollars Invested Method serves as a middle ground between the two, and allows the dilution to be shared amongst the Seed investors, Series A investors, and founders.

Why Are Convertible Notes Used By Startups?

Convertible debt has obvious advantages in that it can allow you to get deals done faster. By giving your first investor(s) a good deal, you compensate them for taking a risk on your team by allowing them the option to take a future stake in your company at a discount, while protecting their downside risk. However, you should be warned that these early benefits can come with nasty long-term consequences if you are careless with convertible notes. It’s best to be careful, do your research, and understand the terms so that you’re protected for future rounds.

When Should Convertible Notes Be Used?

When they can help you close your seed round faster:

If a company is trying to raise a seed round, one of the biggest challenges they’ll face is getting the first investor to say yes. There is an old saying in the startup world that the most common question investors ask is ‘who else is investing?’ There is a ‘herd mentality’ stereotype that is often applied to VC’s.

Even though it drives founders crazy, investors have a point. Startups almost always need cash to succeed, and if they’re not fundable, they’ll fail. For an investor to see a return, the company will need many other investors to see the same value.

No investor takes more risk in this regard than angels or early stage VC’s. They need to take the first chance on a company, typically long before it has any substantial financial or user data to make a convincing funding argument that’s based on fundamentals. Angels are making high risk bets on an idea, a team, and a market. Convertible notes allow founders to provide better deals to investors who take this risk, and ultimately give you a chance to scale your company.

To give you more time to determine a valuation:

One of the most difficult problems when getting an early stage deal done is agreeing on a valuation. Seed stage founders don’t have much data to help price their company, and every investor wants to wait until someone else agrees on a given valuation to get on board. Investors keep the company arms length, waiting for another fund or angel to take the first step.

With convertible notes, founders can offer better terms to an investor who writes the first check, and delay having to put a firm price on their company. Notes also enable companies to avoid extra legal fees associated with negotiations that take place during equity financing . This allows them to save cash and get deals done faster (although there are now templates like Series Seed documents that make this easier).

When Should Convertible Notes NOT Be Used?

When they can overcomplicate your cap table:

If a company raises money with multiple convertible notes, the cap table can get complex and the founders may place themselves in an uncomfortable position. This is especially the case if they don’t hit the next qualified financing on time. Convertible notes are still debt prior to their conversion. You may be liable to pay back cash that you don’t have if your future round doesn’t go as planned. This also gets awkward if founders don’t raise another round of funding at all (i.e. if the company gets acquired, hits profitability, or goes out of business). The key is to remove the complexity by trying to include these scenarios in your thinking prior to closing the seed financing. We suggest reading more about this from Jose Ancer on his insightful blog: Silicon Hills Lawyer.

When they come with extra dilution and liquidation multiples:

We touched on dilution in convertible note conversion earlier in this post, but they can also pose another challenge: liquidation multiples. Here’s a quick example on how a hidden liquidation multiple can surface with a convertible note:

Let’s say an investor who gives us a convertible note worth $1M at a $10M valuation cap (more math to come later). If we raise a $20M seed round, this investor ends up owning roughly 10% of a company that is now worth $20M. They only paid $1M, but now are entitled to $2M in the event of a liquidation. This investor will now receive 2x what they paid in the event of an early liquidation that is worth less than the initial valuation. This is quite disadvantageous for the founder (and potentially other investors). You can avoid this situation by adding some additional language to your convertible notes – similar to this this paragraph suggested by Mark Suster (but consult your lawyer first).

Related Resource: Everything You Should Know About Diluting Shares

What the pros say:

Many investors, such as Jason Lemkin, Fred Wilson, and many others have been critical of convertible notes. They would rather put a price on the company and believe that, due to their experience, they can negotiate a fair price quickly. They also argue that the valuation cap essentially puts a price on the company by default. If you’re willing to price your company, why not just raise the equity and avoid the headache that can come with the conversion? Jason Lemkin also argues that investors who invest with convertible debt are less incentivized to be involved early on. After all, they don’t yet have any control or stake in the company. To some investors, the complexity of convertible notes is not worth the time saved – it’s simply pushing important conversations down the road while exposing both sides of the table to unnecessary risk.

Convertible Note Examples

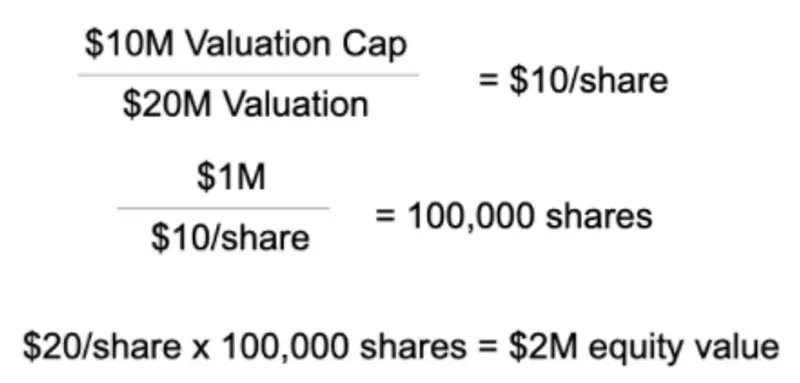

Let’s say you’re a founder of a seed stage company who just raised $1M via convertible note. The valuation cap is $10M and the discount rate is 20%. Then, you raise a Series A round 18 months later at a $20M valuation. If there are 1M shares outstanding, then new investors will pay $20 per share, while the investor who issued the convertible note will receive equity based on either a valuation cap or the discount – typically whichever is most advantageous for the investor on a price per share basis.

Example 1 - If the note converts based only on the $10M valuation cap, then the $1M invested will convert into a $10 per share price vs a $20 per share price ($20/share multiplied by ($10M cap divided by $20M Series A valuation), turning the $1M investment into $2M in simple terms. The $1M investment will now convert into 100,000 shares. The seed investor will get an effective 50% discount on the shares ($10/share vs $20/share) and a 100% return on their investment.

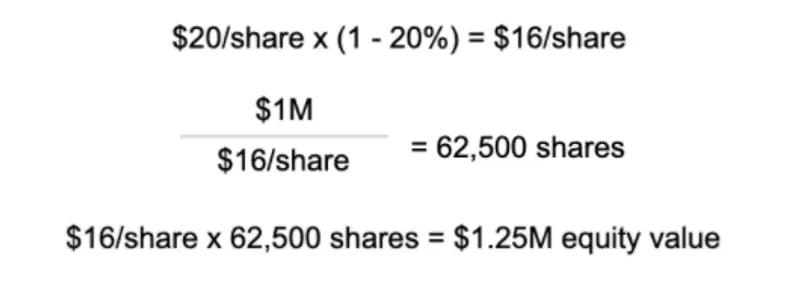

Example 2 — On the other hand, if the note converts at the 20% discount rate, the investor will be able to buy the shares for $16/share rather than $20/share. This would allow the investor to convert their $1M investment into 62,500 shares ($1M / $16/share) rather than 50,000 shares had they invested in the Series A. The $1M investment converts into equity worth 1.25M, a 25% return on their investment.

In this case, the investor would convert the shares on the basis of the cap, because it provides better economics. The math works out similar to what would have happened had they simply invested $1M at a $10M post money valuation, but they did not have to bear as much risk as typical equity holders and likely got less dilution. The investor, in exchange for taking an early chance on a company, gets a better deal than those who came in later. This is an overly simple example of how a convertible note works, but it’s useful to see how the conversion math looks in practice.

Looking for more resources on fundraising, investor updates, and navigating the unsteady waters of startups? Subscribe to our newsletter — The Visible Weekly, Curated resources and insights delivered every Thursday.